Reading the Particulars of Claim and transcripts from the FCA test case proceeding in the UK, I learned about another important difference between the test case and the US cases. The scope of the test case is limited to non-damage policy wordings. That means the court in that case will not address potential interpretations of “physical loss of or damage to property” and similar wordings that insurers rely heavily on in the US cases.

For example, in Gavrilides Management Company et al. vs. Michigan Insurance Co., the presumptive first Covid-19 insurance coverage case decided in the US, Judge Joyce Draganchuk granted the defendant insurance company’s Motion for Summary Disposition. Judge Draganchuk granted the motion on the procedural grounds that the plaintiff failed to allege any “physical loss of or damage to” property, not on the merits of the argument that there was “physical loss of or damage to property.” Nevertheless, she made her views of the merits of that argument plain. Watching the video of the argument on YouTube, I heard her say (as the transcript confirms), “The plaintiff just can’t avoid the requirement that there has to be something that physically alters the integrity of the property. There has to be some tangible, i.e., physical damage to the property.” I heard that as suggesting that she didn’t think restaurants could make that showing. Judge Draganchuk was unimpressed with the argument that “the physical requirement is met because people were physically restricted from dine-in services,” calling it “nonsense.”

Because the plaintiff didn’t allege physical loss or damage, Gavrilides doesn’t tell us much about how other cases or judges will come out. Our reading of the motions to dismiss and other documents filed in other cases shows that there are many different arguments (and defenses) courts have yet to hear. Moreover, case law interpreting the “physical loss” and/or “physical damage” requirements is still relatively undeveloped in the US, and some lawyers claim that it differs between states. Such causal requirements are likely to be the center of gravity in many cases in the US, but the UK test case won’t provide much, if any, guidance on that issue.

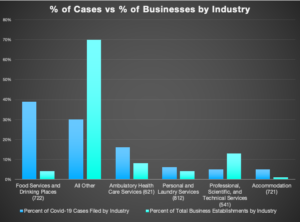

Food Services and Drinking Places are leading the pack, with 40% of the cases, followed by Ambulatory Health Care Services with 16% of of the cases. Most of the ambulatory health services plaintiffs are dentist offices (59 out of the 87 cases in that category). The share of cases represented by other industries quickly falls off after these two.

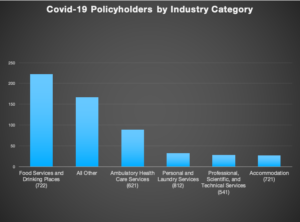

Food Services and Drinking Places are leading the pack, with 40% of the cases, followed by Ambulatory Health Care Services with 16% of of the cases. Most of the ambulatory health services plaintiffs are dentist offices (59 out of the 87 cases in that category). The share of cases represented by other industries quickly falls off after these two.