Author: Jordan Einstein Date: 12.04.20

Over the past eight months, Covid-19 has forced countless businesses across the country and around the world to shut down their operations. Virtually every industry has been impacted, and professional sports leagues are no exception. According to a complaint recently filed on behalf of Major League Baseball (“MLB”) and all 30 MLB clubs in Alameda County Superior Court, the league and its clubs have suffered billions of dollars in losses due to Covid-19. MLB and the clubs filed business interruption claims with their insurers under their “All Risk” policies. The insurers issued blanket rejections of these Covid-19 coverage claims, carefully cultivated to avoid absolute statements, while simultaneously denying claims on a broad basis.

After taking their time to prepare a strong opening pitch, MLB and the clubs filed suit seeking declaratory relief and money damages in state court, traditionally a more welcoming home for policyholders than federal court.

MLB is far from the first business to file suit against their insurers for business interruption coverage. The Covid Coverage Litigation Tracker is aware of more than 1,400 such cases filed in state and federal courts since March. We estimate that several hundred more have been filed in state courts but have yet to be identified due to the imperfect state case identification process.

In fact, this complaint is not even the first by a professional sports organization nor the first baseball-related case. The Houston Rockets and Atlanta Falcons have both filed suits in Rhode Island state court, and several Minor League Baseball cases are currently pending, with one MiLB case already been resolved in favor of the insurers due to the presence of a virus exclusion in the policy at issue in that case. Despite their first win in one minor league case, insurers are still in the early innings of a long legal battle for pandemic-related losses and as one might expect, MLB came out swinging in their 66-page complaint.

As I explained in a summer blog post about the first MiLB case, the sports-related cases for business income coverage do not differ radically from cases in other industries. The central, hotly contested issue is whether Covid-19 causes “physical loss or damage” to property, but each case’s outcome depends on the specific language contained in their insurance policy. As the Tracker shows, insurers have had the upper hand in judicial rulings thus far. But most of the dismissals result from defective pleadings or the presence of strongly worded exclusions in the insurance policies at issue that specifically refer to losses from viruses that cause disease.

The MLB complaint is crafted to avoid these pitfalls. Consequently, the case has a strong chance of surviving a potential motion to dismiss the case. Assuming the case does not get dismissed, MLB will have the burden of proving that Covid-19 does indeed cause physical loss or damage to property; if so, defendant insurers are potentially on the hook for billions of dollars in coverage, unless they can prove that an exclusion or sub-limit applies.

The key Factory Mutual insurance policy at issue appears to contain what the CCLT classifies as a “hidden virus exclusion” as well as “specific coverage for communicable disease.” A “hidden virus exclusion” is an exclusion for pollution, or as here, “contamination” where the policy defines “contamination” to include “virus[es].” “Specific coverage for communicable disease” means exactly what it says – the insurance policy provides specific coverage for losses due to interruption by communicable disease.

Courts have not yet addressed the merits of specific communicable disease coverage provisions, but of the five buckets in the CCLT database, specific coverage is the most favorable coverage bucket for policyholders. Indeed, the MLB complaint alleges that this communicable disease coverage undermines the insurers’ assertion that the hidden exclusion applies, because the specific coverage implies that covered communicable diseases are distinct from the viruses referenced in the contamination exclusion.

Given the importance of the physical loss or damage requirement, it is no surprise to see so much discussion of physical loss and damage in the complaint. The league relies heavily on an assortment of scientific studies pertaining to Covid-19 fomites and their persistence on objects and surfaces, in the air, and their ability to spread through HVAC systems. Moreover, the complaint details government shut down orders, as well as those imposing gathering limitations that specifically refer to the physical loss and damage caused by Covid-19.

Note that the previous sentence reads: “physical loss and damage” as opposed to “physical loss or damage.” Unlike most complaints, MLB consistently uses “and” instead of “or.” The slight phrasing variation could prove important and signify a change in future Covid coverage pleadings. Insurers’ use of the disjunctive “or” in their insurance policies suggests that loss and damage are distinct. As such, MLB need only prove one of the two. Yet MLB asserts that Covid-19 causes both physical loss and physical damage, suggesting that they are marshalling the evidence and arguments to prove both, increasing their odds of success. The following quoted paragraph is excerpted from the complaint and provides a very basic example of the difference between damage and loss.

“The presence of the coronavirus and COVID-19, including but not limited to coronavirus droplets or nuclei on solid surfaces and in the air at insured property, has caused and will continue to cause direct physical damage to physical property and ambient air at the premises. Coronavirus, a physical substance, has attached and adhered to Plaintiffs’ property, and by doing so, altered that property. Such presence has also directly resulted in loss of use of those facilities.”

Here, the physical adherence of droplets and nuclei to property and in the air physically alter property and thus, constitute physical damage to property. Conversely, the last sentence states that the presence also resulted in “loss of use” of facilities which constitutes “physical loss.”

Just as an umpire’s view of a pitch a mere inch off the plate can determine the outcome of a playoff series, a judge’s interpretation of a single phrase, or even word, could determine the outcome of this case. Perhaps then it is fitting that these cases rest in the hands of judges, whom Chief Justice of the United States John Roberts so aptly compared to baseball umpires.

Other Interesting Notes from the Complaint

- According to the complaint, Factory Mutual covers 60% of the Insurers’ total limits of liability, AIG covers 30%, and Interstate Fire & Casualty Company covers 10%.

- Plaintiffs include all 30 MLB Clubs, the Office of the Commissioner of Baseball, MLB Advanced Media, MLB Network, and Tickets.com.

- The complaint alleges that Covid-19 was physically present at every plaintiff’s property.

- MLB asserts eight total bases for coverage including: Time Element Loss, Civil Authority Coverage, Ingress/Egress Coverage, Leasehold Interest and Rental Insurance Coverage, Contingent Time Element, Crisis Management Coverage, Communicable Disease Coverage, Protection and Preservation of Property Coverage.

- According to the complaint, policy limits apply on a “per occurrence” basis, providing up to $1,635,869,608 in coverage for any single occurrence and potentially more for multiple occurrences. The AIG Policy’s Crisis Management coverage is subject to a $10 million sub-limit, but it applies on a “per occurrence” basis and sets no aggregate limit.

- The complaint provides some background and detail about the extent of financial losses, including some explanation of the league’s and clubs’ various revenue sources.

- The outcome of this litigation may significantly impact the operations of the league and individual clubs and may even reach player contracts. If clubs recover their losses through insurance, they will have more to spend in Free Agency.

- The Atlanta Falcons case was actually filed several weeks after the MLB complaint.

- MLB is represented by the Covington and Burling law firm.

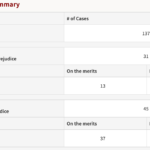

Apologies for the small size (we’re working on adding this in dynamic form to the CCLT website), but what the snapshot shows is that 137 cases have been voluntarily dropped, most often before a response to a motion to dismiss is due, 45 case have been dismissed with prejudice, and 31 cases have been dismissed without prejudice. My impression (not thoroughly checked) is that all of the dropped cases are business interruption cases. That means that more than 15% of the business interruption cases in our database no longer are active.

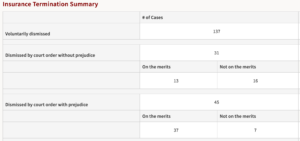

Apologies for the small size (we’re working on adding this in dynamic form to the CCLT website), but what the snapshot shows is that 137 cases have been voluntarily dropped, most often before a response to a motion to dismiss is due, 45 case have been dismissed with prejudice, and 31 cases have been dismissed without prejudice. My impression (not thoroughly checked) is that all of the dropped cases are business interruption cases. That means that more than 15% of the business interruption cases in our database no longer are active.